We’re all sick of hearing about the fuel crisis already. But it’s vital for businesses (and people) to understand what the effects of this are to manage the situation. This article is not about what type of car people should have to get to work. Fossil fuels feeds into nearly every part of our lives, a fact that can’t be ignored. So what will the impact be and what will be affected, and what are the flow on effects (and how should we respond)?

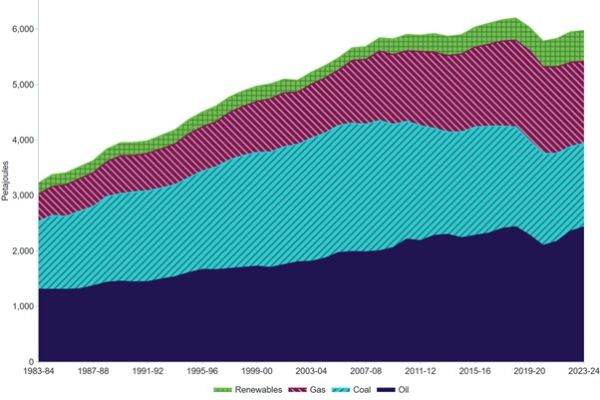

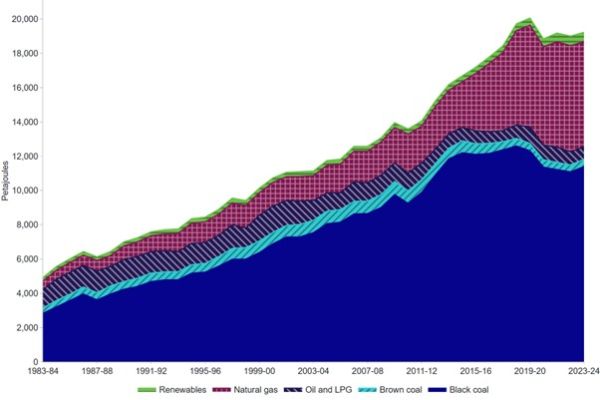

According to the Federal Department of Climate Change, Energy (etc), 91% of our energy consumption comes from Fossil Fuels (see charts below for the 40 year trends). If you look at our production instead, renewables are low single digits and 2/3’s of our total energy production is exported – we don’t use it here but have it available. Power generation and transport are most affected, so I’ll delve into that further down.

What most people miss is that Fossil Fuels, oil in particular, are a part of most things a modern society uses. By no means an exhaustive list, here are some examples of flow on effects:

- Agriculture:

- Fertilisers – The world could learn from Sri Lanka’s April 2021 ban on (fossil fuel derived) fertilisers and pesticides to go “organic”. 7 months later, the country overturned the ban because it caused a severe food security crisis. Yields fell by 40%, incomes by 50%, and a starving population were protesting.

- Diesel – there is a 2 week planting window and the same for harvesting. If farmers can’t keep their machinery moving, the crops are lost. Further, water pumps and other machinery is essential to feed live stocks and crops.

For those that think food comes from a supermarket, either of these shortages won’t be seen on your shelf for maybe 6 months.

- Construction: cement, asphalt and plastic. Just a simple thing like plastic drainage pipes have gone up in price 30-40% already. That’s if you can get them. What people don’t realise is the flow on effect – the project can’t continue when supplies aren’t available. When the job site stops, there are still significant costs including standing down people and machines, re-scheduling other supplies etc. This delays the project, and most contracts have penalty clauses for late completion. Add in that someone is paying interest costs on all the funds for the project, which before long will send the builder or someone in the chain broke. What a terrific outcome when we have a housing and infrastructure shortage already – thereby pushing up rents etc for those who can probably least afford it.

- Transport: most people immediately think of the extra cost at the bowser to fill up their cars. Not to downplay that too much because it is important (there are already reports of an increase in “sickies” because people can’t get to work), but:

- Truck transport – nearly all goods transport (besides a handful of local delivery trucks) is reliant on diesel. At the time of writing, transport companies have fuel levies in place of around 30-40%, adding to the cost of every single good. Suppliers are pushing the supermarkets to pass on (hopefully temporary) cost increases to avoid going broke.

- overseas tourism forward bookings have dropped 70% with the flip side that domestic intra-state bookings have increased by 50%.

- Air & Sea freight – major shipping lines have slapped importers with surcharges (a “rate restoration program”) of $USD300-700 on a standard 40 foot container otherwise costing $USD2,300 (13-30% increase). We had an airfreight quote that went from $14,000 to $18,000 during the day, only to hit $22,000 by the time the booking was finalised the next morning.

- Other products: all the following products use fossil fuels in their ingredients: medical equipment (syringes, IV bags etc), medicines (including aspirin, paracetamol, antiseptics and antihistamines), all types of plastics (anything with the name poly in it), clothing and textiles, personal care (shampoo, shaving cream, lipstick, deodorant), paints, detergents, lubricants, PPE, water treatment. Nearly all earthmoving, farming equipment, and marine equipment use fossil fuels for both fuel and lubricants, as do wind towers.

- Rubber and iron get a special mention in this post because of their prevalence in our industry. A supplier advised this week that all rubber products have had material cost increases of 50-60% (not equal to total product cost increase in many cases), which will take about 4 months to flow through.

The worst part in this whole sorry saga is that this is TOTALLY SELF INFLICTED. Decades of negligence from our politicians and bureaucracy have created this mess. We have nobody to blame but our own lack of preparedness, because whether war, disease, natural disasters, strikes or trade blockades (like from China a few years ago) there will always be something. 20 years ago, we were 90% self sufficient for our fuel needs, and had 11 refineries. We now have 2 (both scheduled for closure in 2027) and only 10% local capacity. And not only were many warning of this (such as the late Jim Molan and even the Governments own Productivity Commission), it was heard but not acted upon.

In fact Covid should have taught us all about supply chain management and how critical self sufficiency is. In 2020, the Morrison Government did a small amount of repair work (buying up 1.7 million barrels of oil albeit stored in the USA because we have no storage facilities). In 2022, the Albanese Government sold this off for a $AUD230 million profit (probably the only thing they’ve ever sold for a profit) – to give away with their renewables subsidies…

There have been plenty of warnings. The International Energy Agency advises all nations to keep a minimum of 90 days fuel reserves. Most other places have heeded the warnings, with Japan at 250 days, anti-oil France at 108 days, and even our NZ cousins at 50 days whilst Australia is around 30 days. We could have also learned from our largest trading partner China: they have 2.4 billion drums in reserve 50% privately owned and 50% Government – enough for 6 months, and are smart enough to diversify their supply chain with 20% through the Strait of Hormuz, 30% from Russia, some domestic (10-20%) and the rest elsewhere.

The Singaporean President in 1980 warned that Australia would become “the white trash of Asia”, a prediction that came true this week when our Prime Minister came out with his begging barrel to try to ensure this small island nation (using crude from the Strait of Hormuz) could keep supplying us. The greatest irony is that Albanese’s only bargaining chip was to offer another fossil fuel (gas) in exchange – very Freudian for a Government that demonises fossil fuels. Add in that Aviation fuel is probably in shortest supply and the rest of us are being asked to conserve fuel and stay home, one wonders if he’s heard of video conferencing?

This made me think: how can a wealthy (high incomes) island country with no natural resources and a population 20% of Australia’s provide us with fuel more economically than we can? Looking at the supply chain:

- Singapore – buys crude oil from the Middle East, loads it onto ships and sails it all the way to Singapore, unloads, transports to their refineries, refines the fuel, send it back to a ship that then goes all the way to Australia, and has it unloaded in the most costly ports in the world to go into a local storage facility before being sent to point of usage. Note also that Australia doesn’t have a single ship to second to transport fuel or any other bulk commodity due to over-the-top regulations and costs (meaning we are fully exposed to foreign powers for everything)

- Australia – has plenty of oil fields in Australia (WA, Taroom in Qld, offshore, Gippsland Basin (Vic), Cooper-Eromanga Basin (SA/Qld), Otway Basin (Vic/SA). All we’d need (apart from extraction) is local refineries, which by the above non-exhaustive list of areas means we could have in each state to spread risk. The products could then go from the refinery (with local storage) straight to point of usage.

Can anyone please explain how the Australian option could possibly be more expensive? And if you can, please tell us what we can reduce to at least equalise our cost?

One touted explanation is lack of scale and small domestic market. Singapore’s domestic market is a fraction of ours, and they compensate by exporting (something we must do to build our wealth). I get the scale argument, but surely it can’t be that great?

Other actions we can take is to supplement with biofuels and oil derived from coal and other products. I don’t know enough about that to write about it. I do however trust Judith Sloan’s information (Economics Commentator in the Australian) when she says that to build up 90 days of fuel reserves in Australia (storage, product and all associated costs) would cost about $20 billion over 4 years (and that is not money spent, having the oil is an Asset on any balance sheet). Her estimate of the cost of that is maybe 10 cents per litre, which based in the weekly fuel cycle we wouldn’t really notice. The additional supplies should all be developed locally also, actually building our wealth and self sufficiency at the same time.

In fairness our Government recently relaxed the sulphur content to increase supply. One reason we pay more for diesel is that we use Ultra-low sulphur diesel which makes the fuel more expensive (estimates are 2-20 cents per litre) than in countries where they don’t impose that requirement (this has a legitimate environmental impact, significantly more important compared to CO2 emissions). So I thought I’d look at why diesel in particular costs so much in Australia.

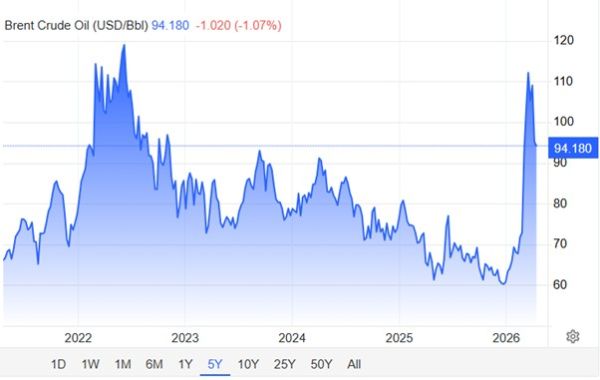

It’s not surprising that the highest increases in the retail cost of fuel has been in countries with relatively low reserves, Australia being one of the worst affected. Nobody can explain why diesel now is about 50% more expensive to buy at the bowser ($3.20 versus $2.20) than it was at the last peak brent crude oil price (see below 5 year Brent Crude Oil pricing) which was HIGHER in 2022 than it is now. Supply and demand will do that, especially when there is no confidence of any real and sustainable actions being taken to improve the short, medium and especially long term supply.

The other interesting observation is that petrol pricing now is about the same as the high point over the past few years (about $2.20 for regular unleaded). Diesel is normally about 20 cents per litre less, but has now been stuck at about $3.20 per litre for a month. Australia’s biggest toothless tiger (the ACCC) continues to find nothing wrong with fuel prices jumping around 50 cents from one day to the next, even though it takes 3-6 weeks for any price change at an overseas refinery to flow through to our bowsers. Hard to call that anything other than price gouging. I’m against price manipulation and definitely against Government rules on pricing, but maybe we need a rule that no product price can be increased or decreased by more than say 5% over the course of a week?

Continuing on the same path that led us here is clearly the wrong strategy. Only uneducated ideologues could possibly turn a blind eye to what has caused all this, let alone to double down on the current pathway. The only way forward is to do what all other nations are doing: understand that fossil fuels are possibly the biggest contributor to a wealthy and healthy civilisation, drop all the market distortions and subsidies, and remove the hurdles to using our own natural resources (that we export to others) for our own benefit instead. Drill, baby, drill. We must support oil, gas, coal and even nuclear as it underpins any modern economy.

Australian Energy Consumption – by fuel type

(Source: Australian Department of Climate Change, Energy, the Environment and Water)

Australian Energy Production – by fuel type

Brent Crude Oil Chart – 5 Years (Source: https://tradingeconomics.com/commodity/brent-crude-oil)

Words from the wise

“Those who fail to learn from history are doomed to repeat it” – Winston Churchill.

“The Australian sun cannot be interrupted by a war or anything else” – Chris Bowen, Energy Minister for Australia…

Except of course: the earth’s rotation causing darkness half the time; clouds and other shade cover fluctuating every second; weather events like hail damaging panels; relies on other stable energy supply to keep the grid from “doing a Spain” and collapsing; and nearly all hardware sourced from China, that has stopped product supply to/from Australia before, and even has the capacity to remotely shut solar down (they have already done this in the US).

Oil doesn’t have to travel the Strait of Hormuz either, if we were smart enough to use what we have in our own country ourselves…

As always, Onwards and Upwards!

Fred Carlsson

General Manager